China is home to some of the world’s largest, most successful and innovative internet-based companies, e.g. Alibaba and Baidu. As of the middle of 2018, 9 out of 20 of the largest tech companies in the world, by market valuation, were headquartered in China, with the other 11 based in the U.S. Almost no consumer-facing business in China can succeed without an online and offline strategy today. Perhaps because consumers are still new to traditional Western ways of shopping or banking, Chinese consumers are very willing to switch to buying online.

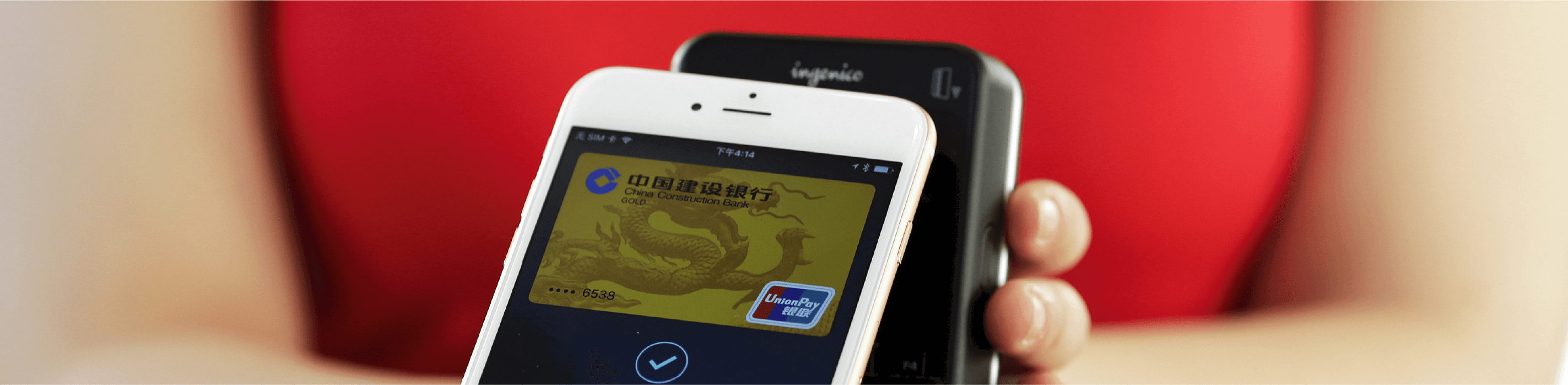

In China, 600 million people will use their phones to make mobile payments as of the start of 2019, about 550 million people will regularly use their phones to shop online. As online firms keep on growing, they will likely find more and more success in China. The value of mobile payment transactions in China reached $12.8 trillion in the first 10 months of 2017. This compares with an estimated $49.3 billion worth of mobile payments in the U.S. during the same period. The sheer size of China’s markets, as well as users’ receptiveness to trying out new ideas, may make it the venue of choice for trying out new digital concepts.

The online share of retail in China, at 12.4% in 2014, 28.6% in 2018 and projected to be 33.6% in 2019, is higher than it is in the U.S. and is not close to reaching saturation. Many retailers will adapt, often with far fewer physical locations. The impact of all of this on employment is just starting to appear, but many millions of sought-after white-collar jobs will be eliminated in the next few years. When you couple this with the fact that, in terms of population, more than 50% of China is now urban but there are still 10 – 15 million people a year moving from the countryside to the cities, there is likely to be an increasing unemployment issue in China that will need to be addressed.

A final point to consider within the digital sector is how Chinese companies view IT services. Finding the CIO in a Chinese company is often hard, especially in a state-owned enterprise. A typical Chinese company spends only 2% of revenue on IT versus international benchmarks of around 4%. As these companies struggle to bring technology into the core of their operations, they need massive amounts of help to do so. The cost of good IT talent is already soaring. Most Chinese companies will be unable to solve their technology challenges for themselves.

Whilst having done little to address the issue of diminishing white-collar jobs, China has grown its pool of medium and high skilled workers by investing in universities. However, of the 7 million graduates each year, maybe only 3 million find jobs that require a degree. Like graduates all over the world, they largely lack workplace relevant skills. Once graduates are hired, retention of high performers often depends on a highly variable compensation structure and dismissing underperformers.

These remainders who are unemployed or dismissed are a growing segment of society and will be becoming increasingly unsatisfied and disenchanted with the nature of employment. This presents a great opportunity for foreign companies and investors in the Chinese market. However, it is worth remembering that, unlike in Asian counterpart Japan, loyalty to an employer is often low on an individual’s priority list. As such, turnover will likely be high and should be planned for.

It is no secret that manufacturing processes are shifting to surrounding countries, like Vietnam and Bangladesh, due to rising wages in China. Nonetheless, China still enjoys cost advantages in two major talent categories: research & development and marketing & sales. However, it is becoming increasingly common practice to hire midcareer executives in almost all industries. As such, there is an ever-deepening pool of talent available for such industries. Both Chinese and global search firms have rapidly growing businesses that serve local and international companies to address this issue.

China also provides several incentives for overseas Chinese to return. With a population of over 1.3 billion and a rising dominant language in Mandarin (nearly 1 billion speakers), coupled with a fast-growing economy and a rising middle-class – by 2022 more than 50% of urban households should be in the middle class, an increase of more than 100 million households – the result is a vast home market with exposable income.

As mentioned earlier, more than 76% of assets in China are owned by the government, meaning people own less than a quarter of assets. This means that if you wish to do business in China, you’re more than likely going to have to negotiate with the state. The bureaucracy involved in negotiating with the state can slow down the pace of business ventures. Joint ventures are difficult to establish because they have substantial government involvement. Legal matters lack consistency and can be changed at the will of the Chinese government. However, in recent years they are trying to upgrade legal protections making the business environment more enticing to foreigners.

If regulations require you to have a joint-venture partner and a minority position today, it is best practice to assume it will be that way forever in the core business activities. So, if you don’t find that model attractive today, do not invest in it in the hope that it will change tomorrow. Organisations ought to closely follow the evolution of government policy and align your stated intent with such policy as far as possible. Using the words from the government statements in your own statements communicates your commitment to China. It is important to be clear if you are in China for the opportunity in China or if you are there for the opportunity that China creates for you in the rest of the world.

All the while it is best to bear in mind that corruption in China has certainly become more of an issue as the Communist Party of China’s policies, institutions and norms have clashed with recent market liberalisation. Bribery, kickbacks, theft and misspending of public funds cost at least 3% of China’s GDP each year. Because the Chinese government owns the majority of China’s assets, they have the ability to spend without much oversight into the budget process. Recently there has been a crackdown on corruption and many high-profile political figures, such as Sun Zhengcai, have been jailed for getting caught up in the net of bribery, abuse of power and other corrupt practices.

The arrest of Huawei’s CFO, Meng Wanzhou, in Canada at Washington’s request immediately raises the prospect of like-for-like retaliation against executives from North American companies, a fear reinforced by the arrests of a former Canadian diplomat turned NGO researcher and a Canadian businessman. Western business people are ensnared in low-level court proceedings in China far more regularly than is reported in the West, however, the risk remains low of a retaliatory move against a Western executive of similar status to Meng.

For every U.S. tech company and Western multinational, especially those critically reliant on Chinese sub-contractors, their value chain is now actively at political risk. Local suppliers and their sub-contractors are susceptible to pressure to behave ‘patriotically’ when authorities convey the message, however tacitly, that lack of cooperation with foreign multinationals is in the national interest. Companies need to take urgent steps to measure their potential exposure to these risks. Doubling up value chains, including alternatives outside China, would mitigate the risk of political and regulatory disruption.

Additionally, when you couple this with Trump’s isolationist ‘America First’ policy, Chinese companies will be compelled to seek alternatives to the U.S. in response to Trump’s tariffs, further accelerating the changes to regional trade and the value chains that support it. The overall effect will be that more value chains will begin and end in China rather than beginning in China and ending in the U.S. Burgeoning middle-classes in China and South & Southeast Asia provide a growing market for China’s consumer and industrial goods. There will be fewer global value chains and more regional ones.

Regional value chains do have an advantage: they are shorter than global ones. As global value chains have gotten longer and leaner, they have grown more fragile, just as the pressures on them are increasing from the technological change. The Trump administration’s trade policies will provide new impetus to the developing patterns of multiple, shorter regional value chains.

In the longer-term, it is worth noting the increasing Chinese military power. Until recently, China had never been a naval power – its large land mass, multiple borders and short sea routes to trading partners, it had no need to be and, as a consequence, it has rarely been ideologically expansive. However, this is all changing in front of our eyes.

China has been laying the groundwork for superpower confrontation in the South China Sea. In 2017, China constructed 290,000 sq. m. of dual-use civil-military facilities on the Spratly and Paracel Islands in the South China Sea. On the face of it, this may seem to be a local dispute over fisheries and oil fields but in actual fact it has much broader implications. Each year $5 trillion in commerce – nearly one third of global trade – passes through the South China Sea. China’s military build-up now allows it to project power across those sea lanes, challenging the freedom of navigation guaranteed by the U.S. Navy for the better part of a century.

When you consider an incident in 2006, it is easy to understand why tensions have been building up for some time. U.S. Navy ships were situated in the East China Sea in preparation for the visit of a U.S. Commander and an undetected Chinese submarine surfaced within 5 miles of the 1,000 ft. USS Kitty Hawk. This incident and the build-up of civil-military facilities are a signal of expansionist intent from the Chinese – “We are now a maritime power, these are our seas”.

Without a code of conduct or an established mechanism for de-escalation in place, sabre-rattling in the seas neighbouring China could spiral into full-scale conflict. This would immediately disrupt the international supply chains on which modern manufacturing depends, causing shortages for many companies.

China are still at least a couple of decades off challenging the greatest maritime power in the world, the U.S. Navy, so any threat of conflict is not entirely imminent. However, China must secure the routes through the South China Sea, both for its goods to get to market and for the items required to make those goods to get into China. As such, political tensions in relation to naval passages are likely to increase in upcoming decades. To mitigate these risks, companies ought to assess these factors when entering the Chinese market and may benefit from looking at the potential for a regional rather than global value and supply chains.

Moving from sea to land, it is important to consider the construction and implication of China’s Belt and Road infrastructure initiative – the creation of an ocean-going highway for goods and a land-based route formed from the old Silk Road route. As Belt and Road expands in scope so do concerns it is a form of economic imperialism rather than an attempt to improve global networks – the geopolitics of fear.

Considering that, increasingly, China’s mind-set is that there are fewer and fewer things to learn from foreign partners and they’re more attracted by how a partner can help them expand internationally, these concerns may be legitimate. The economic strategy of ‘one belt, one road’ is worth keeping an eye on to see how other nations respond to its initiatives and whether they view it as Chinese friendliness or expansionism which, in turn, will affect potential value and supply chains.

It is common for Western businesses to move operations overseas to save on operational costs. However, in China, operational costs are getting more expensive. Companies are also becoming alarmed by the industrial overcapacity. Subsidies have encouraged some firms to continue production even with dropping demand and then sell their products overseas.

Increasing salaries and growing turnover are also a trend around China, especially in second and third-tier cities. Nevertheless, China’s population allows great potential for productivity and potential for demand. As wages continue to increase, so does the purchasing power of Chinese workers. Even with increasing costs, having a business presence in China represents a large opportunity for growth.

Much of the current attention is on the trade disputes between the U.S. and China, but this should not distract from the potential long-term benefits for U.S. companies to engage with China. Nonetheless, when implementing a long-term plan for Chinese market investment, it is vital to keep an eye on the developing disputes between the U.S. and China, whether they develop into fully fledged conflicts or not will make or break a business plan, no matter how meticulously planned out it is.

Technology

How the industrial services will be impacted by digital twin

The meaning of digital twin is still surrounded by a fair amount of vagueness. We will shed some lig...

Carlos Miskinis | Sep 2018

Industry

The benefits of combining regenerative farming with agtech

If we resist embracing change and finding solutions, it is obvious that the damage we are causing wi...

Carlos Miskinis | Mar 2018

Looking at digital twins in healthcare.

More money is flowing to fewer startups. This trend is also mirrored in seed financing rounds, with a 30% decline in total financed seed deals between 2017 and 2018..

Our next workshop is in London in November looking at the adoption of digital twins across the sector.

See how we can support you, contact the healthcare team.

© 2011 - 2026 CHALLENGE ADVISORY LLP, a UK limited liability partnership, is a member firm of the CHALLENGE ADVISORY network of independent member firms. Challenge Advisory LLP is a limited liability par tnership registered in England and Wales with registered number OC380630. SEO by rankunlimitedseo.com Challenge Advisor y LLP