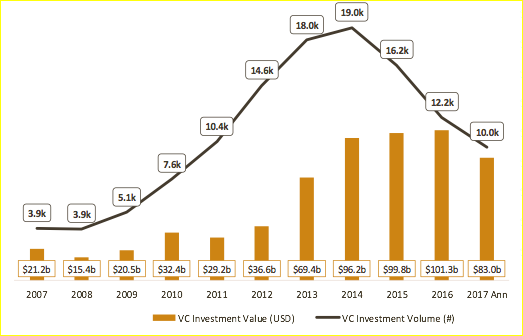

The chart below shows the total VC investment volume, across all stages, has been in steady decline since the peak in 2014. Total VC 2017 deal volume is almost half of the peak.

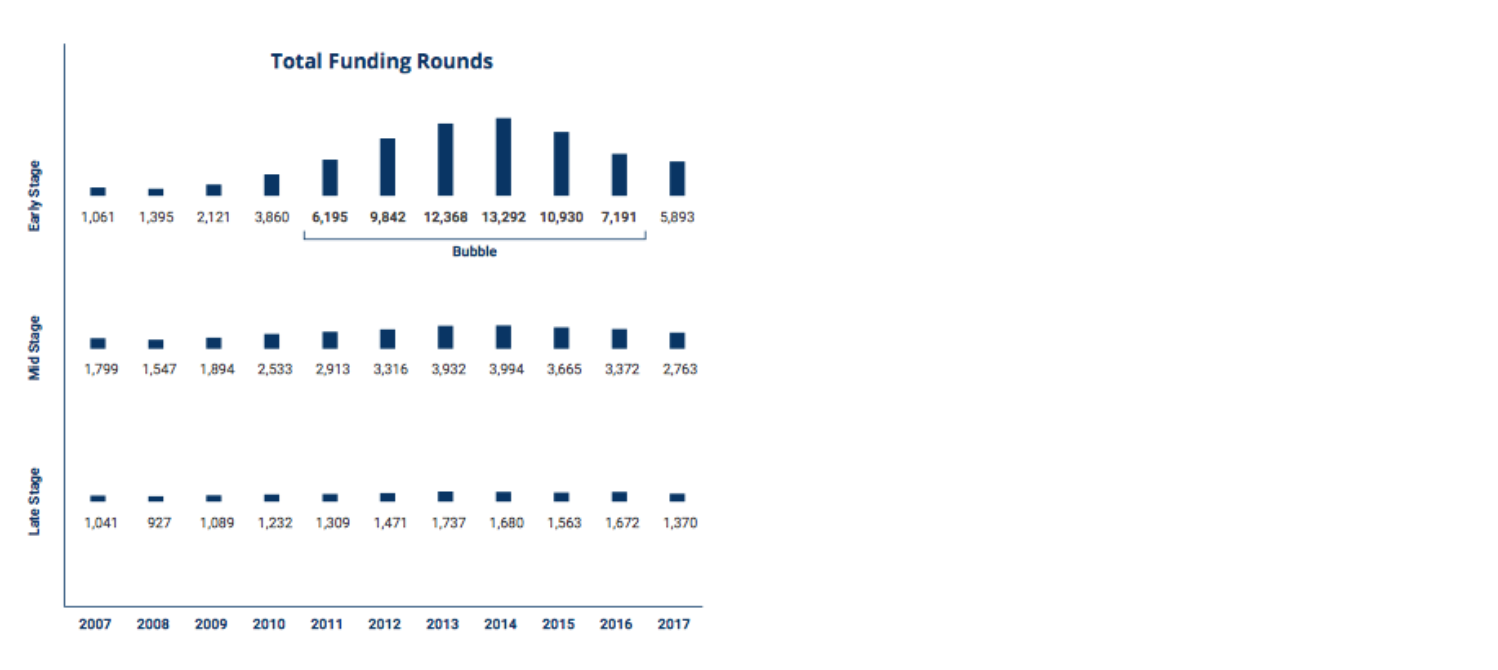

Once we deep dive into the analysis and assess against deal stage, we find the collapse in deal volume has been concentrated at early stage rounds.

Interestingly, as deal volume continues to decline, we find average deal size has increased significantly.

Government innovation policy practice

Why governments need a value capture strategy to realise their innovation efforts

Innovation policy

More money is flowing to fewer startups. This trend is also mirrored in seed financing rounds, with a 30% decline in total financed seed deals between 2017 and 2018.

There have been several attempts to explain this trend. Techcrunch highlights the end of the app era as a main contributor. Our societal shift to mobile was mirrored by VC funding a raft B2C apps which took advantage of consumers emerging mobile first behaviour. As the android and IOS ecosystems became established, the opportunity had disappeared.

Challenge Advisory has noticed a natural rationality had entering VC investors since 2013. The establishment of lean innovation, growth hacking, design thinking, open innovation etc had moved investors away from a spray and pray approach to a diligent, scientific approach to high growth innovation. Evolution, rationality and consolidation were inevitable.

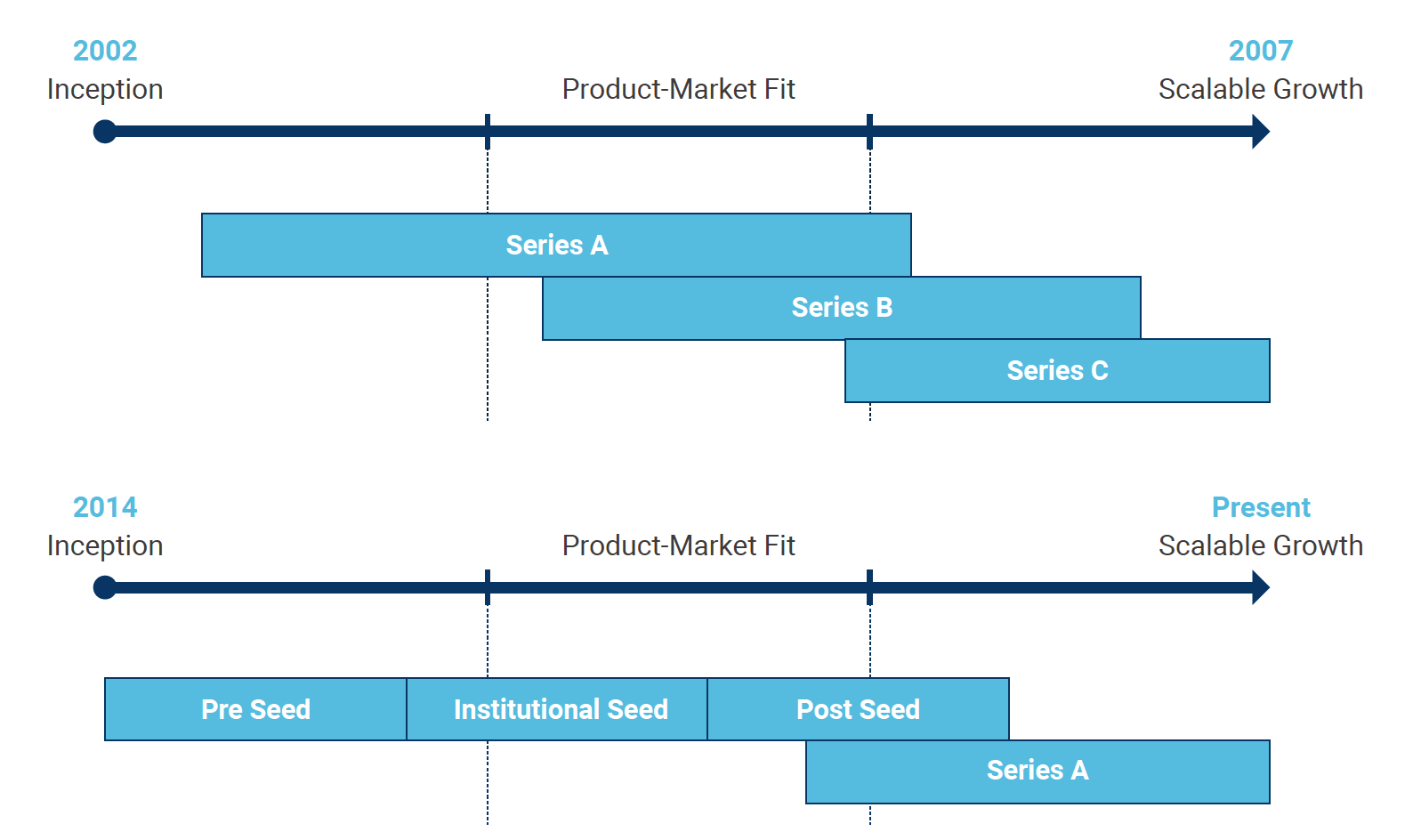

The impact, has been changing investor expectations at different stages of the fundraising process. Startup’s are expected to have firmly established product-market fit prior to a Series A round. Series A and post series A financing are explicitly used for sales and marketing activities to commercialise innovations. The diagram below illustrates how investor expectations have shifted.

Concept money is no longer available at the normal seed stage with investors becoming more strategic in their bets and opting to invest in startups who have found product-market fit. Fortunately a new type of financing has emerged to address concept money needs, pre seed, typically at around the $500,000 mark.

Over $1 trillion in committed capital sits in the coffers of private equity and venture capital funds worldwide. These unprecedented sums are are splits between $145 billion allotted to VC’s and $961 billion to PE. These sums have led to too much cash chasing too few deals in the venture capital ecosystem which is pushing VC funding downstream towards larger sums of capital for more mature companies. A winner takes all environment has been created with the best companies reaching billion dollar valuations after larger fundraising rounds.

In December 2018, the Dow Jones experienced a historic rout with analysts arguing the emergence of a bear market. The tech industry experienced the worst parts of the subprime crisis of 2008, but is the long predicted end of this bull market upon the tech industry? Adding to capital raise concerns are the broader economic issues; $9trillion debt on corporate balance sheets, trade wars, interest rises and slow down in capital markets, slowing on industrial spend etc. For a generation of founders, business frugality is an alien concept, having never experienced the full ramifications of the 2008 crisis. Startups who are dependent on VC funding will experience the hardship, leaving those with strongest balance sheets to survive. Is a correction coming? The dry power, larger funds, raising debt funds, all signal the VC world is preparing for an economic slowdown. Founders must think about their capital requirements for the next 18+ months, and manage raises accordingly.

Government innovation policy practice

Why governments need a value capture strategy to realise their innovation efforts

Innovation policy

Technology

The model of digital twin data and its requirements

The meaning of digital twin is still surrounded by a fair amount of vagueness. We will shed some lig...

Carlos Miskinis | Feb 2019

Industry

For the first time, data can be viewed as a new crop for farmers as it can generate value for them a...

Sam Freedman | Apr 2019

Have a look at our fundraising brochure.

Governments are dedicating resources to areas of strategic value creation, without an effective innovation realisation strategy. .

View our services in fundraising.

Contact the funding team.

© 2011 - 2026 CHALLENGE ADVISORY LLP, a UK limited liability partnership, is a member firm of the CHALLENGE ADVISORY network of independent member firms. Challenge Advisory LLP is a limited liability par tnership registered in England and Wales with registered number OC380630. SEO by rankunlimitedseo.com Challenge Advisor y LLP